Hey there,

since this is a complex matter, let’s start with an emoji-augmented too long; didn’t read:

Tl;dr

This week, the Securities and Exchange Commission (SEC) has filed a lawsuit 👊️ against Kik. 😱 They claim that Kik sold unregistered securities (aka Howey test 🍋) in their 2017 $100m ICO. 💸

I know what you think….ICO….but, but, but ☝️☝️☝️ this was not one of the many shady 2017 ICOs (pre-product 🔎, with nothing but a white paper 💭).

At the time of the ICO, Kik was already a Series D stage startup 💪 with a live messaging product in the market 📱 and mass adoption. 👏 Although daily active users (DAUs) were on the decline 📉, the DAUs were still up in the millions. 🔥 The company had already secured c. $120m in traditional venture funding from some of the top VCs 🚀, including USV and Foundation Capital and later stage strategic funding from Chinese juggernaut Tencent 🥊, the operator of WeChat‼️

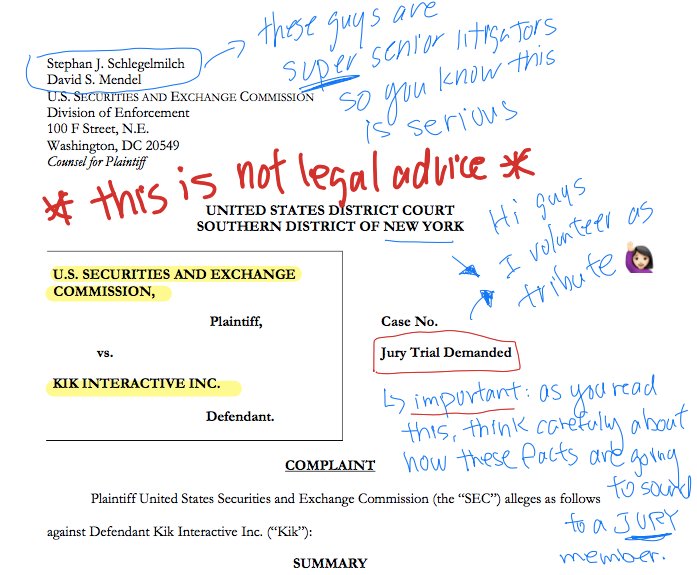

This 49-page SEC lawsuit is an industry-first 🥇

A lot of previous cases and projects have settled with the SEC , but it looks like Kik is actually going to trial with this one ⚔️. The lawsuit doesn’t come unexpectedly: Kik made a public Wells response 📸 (very unusual move, Wells responses are typically private 🤐). They also launched and seed-funded another crowdfunding campaign (with no less than $5m💰, after burning 🔥through another $5m in billables before that) .

…So this week it finally happened, the SEC dropped a 49-page complaint in the SDNY (Southern District of New York) district court 😵. 49 pages is much longer than usual, meaning that the fact-gathering process must’ve been super exhaustive for the SEC 🏋️. If this doesn’t settle, it goes to jury. 🤗🤡🤠

Remember that thanksgiving dinner table when you tried to explain your uncle about bitcoin and ERC-20s? 🙄 You better hope he remembers everything you told him about blockchains ⛓️, because your uncle might now get to sit in the jury and decide on the future of crypto! 😝👨🏻⚖️🙏🏻

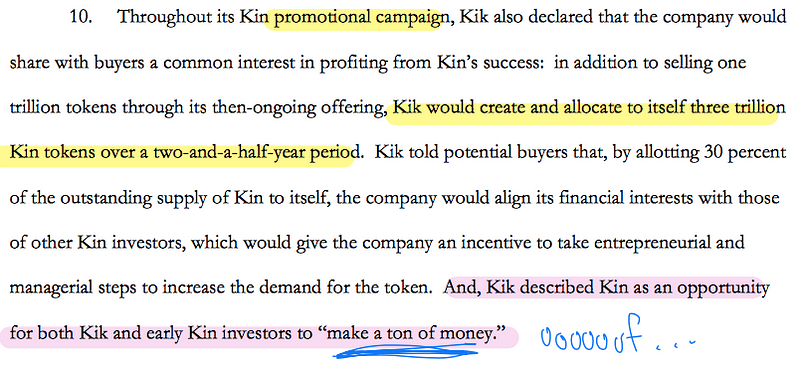

Kik is not your typical 2017 ICO

I remember it well, for a moment there in early 2017, every founder’s dream seemed to come true: raising millions without dilution 🤑. It was a complete fantasy land 🌈 where unicorns were minted with a couple of Solidity lines 🦄 and the entire entrepreneurial activity was concentrated on fundraising rather than on shipping product 🤦♂️. Most of us know by now that for the majority of crypto projects the marketing wrote a cheque, which the tech couldn’t cash 😭. And this is not even speaking about the scammy projects in the space ☠.️

But what if you’ve indeed shipped a super successful product 📦👌🏻, raised from the best VC funds in the world 🕶, all the way to Series D, but the product-market-fit you once had seems to be waning 📉 as consumer sentiment is shifting 👀. Your options of raising another round are tapped out and your runway is coming to an end. This is a situation that every entrepreneur dreads 😰. It’s too late for a product pivot: you either have to revamp growth 📈 or shut down💀.

Such was the story of Kik in 2017, before the company had the idea of “pivoting to digital tokens” as the SEC puts it. This is excerpt from the claim summarizes what was going on in the eyes of the SEC Commissioners:

Katherine Wu produced a really funnily annotated version of the 49-page lawsuit with lots of useful comments and emojis, which you can find here. I’m using screenshots throughout this post to make things a bit more fun to read. 😁 I can also highly recommend this Gimlet podcast episode 🎙️, which I listened to a while ago and which followed Kik during their $100m initial coin offering process.

Kik definitely wasn’t your typical ICO project with no product 💭 and a white paper 🗒 for an abstract protocol 🤓. Rather, it was a late stage Series D consumer app backed by some top-tier VCs 🚀. Their $8m Series A was led by Union Squared Ventures (USV), their $19.5m Series B by Foundation Capital, with participation of USV and Spark. These are some of the best names in early stage VC. The last round, their $50m Series D in 2015, was led by Tencent, the Chinese tech juggernaut and operator of WeChat.

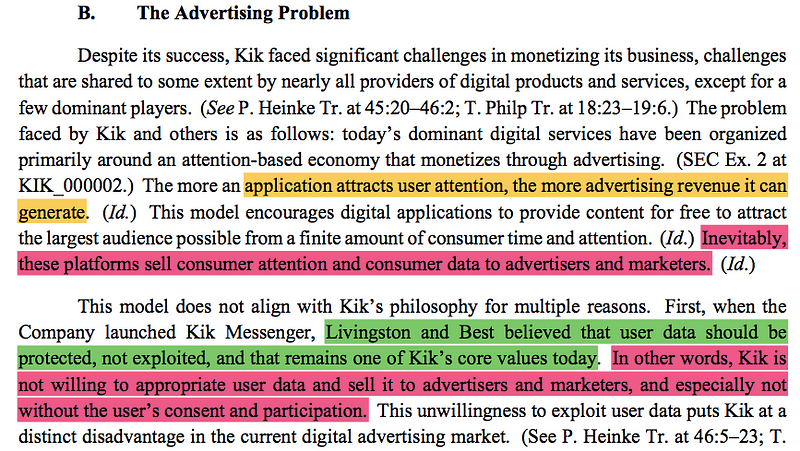

Fight for survival in the attention-based economy

In 2017, Kik was at a stage where you would typically expect an exit or an IPO if traction allows. In fact, in the SEC’s filing it appears that this is what was indeed intended, but which did not materialize:

“In or about October 2016, Kik hired an investment bank to identify companies that might buy Kik. The investment bank contacted 35 parties and signed confidentiality agreements with seven companies that wanted additional information about Kik. By February 1, 2017, however, all seven potential suitors had declined to buy or merge with Kik.”

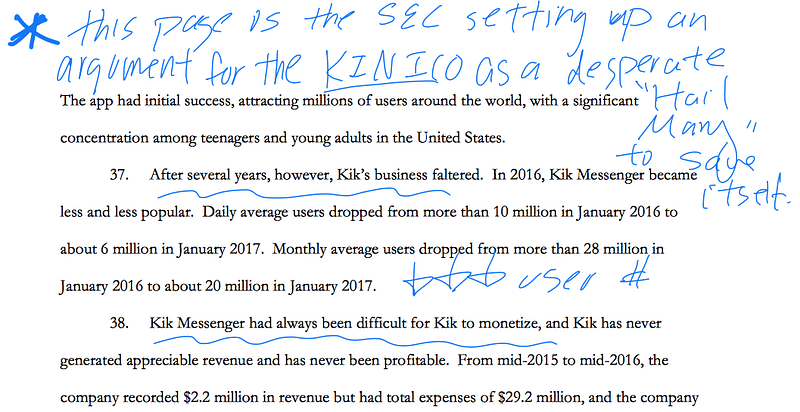

The SEC also uses the drop in daily active users (DAU) and the high burn rate🔥 (not unusually high for late stage social networks!) to build up a “failed startup” narrative throughout the claim (as if social wasn’t the hardest thing to crack ⛏️ in consumer web).

Of course, this is just one side of the story, in the Wells response, Kik acknowledges the challenges faced by the company. They counter it with a narrative that resonates deeply with anyone who believes in a free and open internet that shouldn’t be controlled by a few attention monopolies.

It boils down to the old saying about the ad-based social monetization model: “if you’re not paying for the product, you are the product”. But this still raises the question of whether paying for the product through a token offering is the solution. 🤷♀️ Which brings us to the next point. 👇

“Pivot to digital tokens” or genius product move?

Let’s ask ourselves for a moment that if there were no security laws, whether the token model actually makes any sense from a product perspective. 🤷🏼♂️

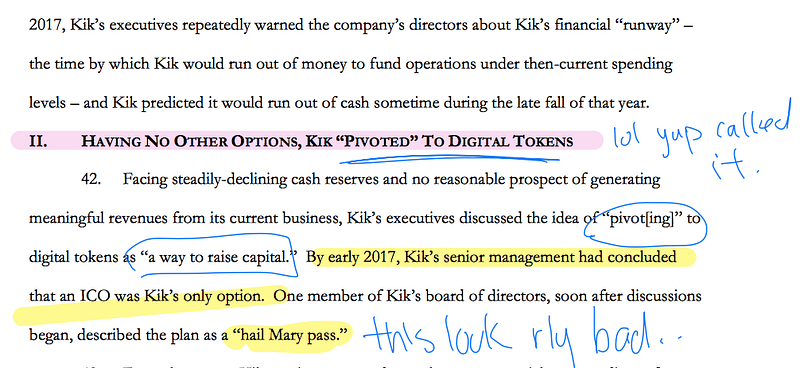

The way the SEC spins the story is that with a monthly burn of $3m 🔥 and a runway to the end of 2017 📆, an ICO was the only way for Kik to escape the fate of the many players in social and messaging (RIP ⚰️ Myspace, Friendster, Socialnet, Yik Yak). They call it a “pivot” to digital tokens. ↪️

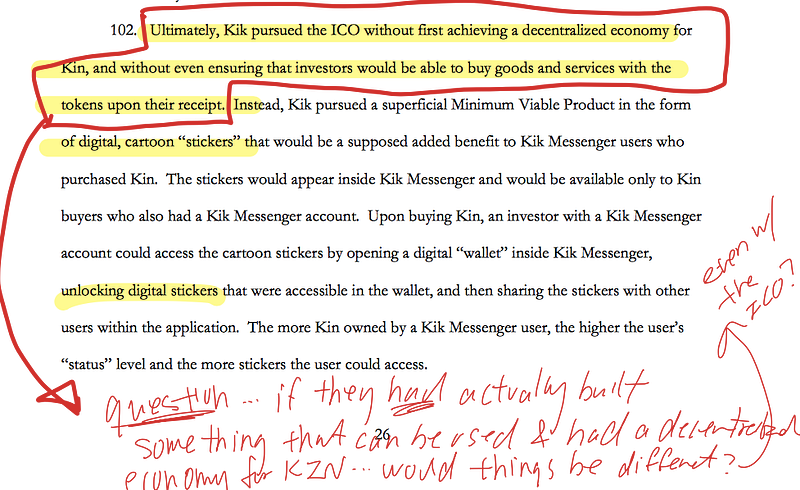

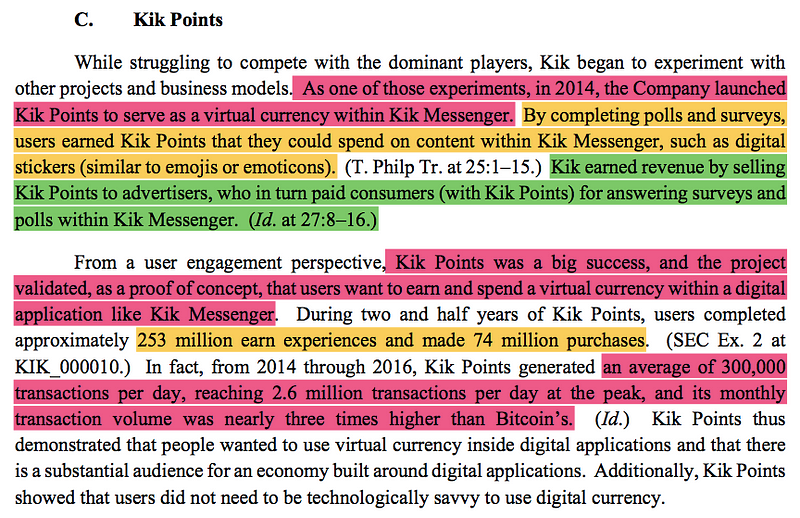

Like many ICOs at the time, Kik hadn’t actually built the decentralized economy it promised to deliver in it’s white paper.

But, but, but ☝️☝️☝️ This part of the SEC argument clearly glosses 💅 over the fact that Kik was by far more advanced than 99% of the crypto projects. They had actually operated a virtual currency, Kik Points 🧿, as early as 2014❗️️ This Kik Points ‘beta currency project’ is detailed in the Wells response:

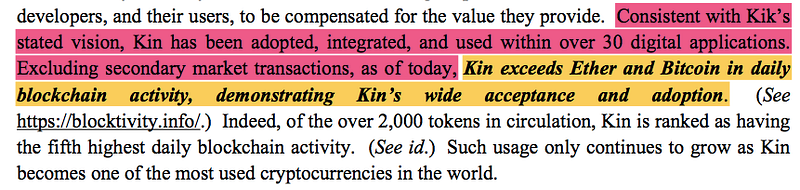

So, even if the SEC later almost ridicules the Kin token by implicitly accusing Kik of launching a $10k sticker pack 😆, the Kik Points example clearly shows that they were already well beyond the vaporware stage of most 2017 ICOs.

Like everyone who ever built anything on the Ethereum chain knows👨🏻💻, scalability was and still is a main hurdle. So, no wonder Kik had the same issues with an application that was supposed to process social-like interactions.

But, but, but ☝️☝️☝️ ️Unlike most ICO projects, Kik actually put the fresh money to use. As the Wells response shows, they actually shipped product after the ICO and the Kin token is in active use today.🤜 That’s so much more than most 2017 projects can claim.

Ok, so some of you might still ask whether a token makes sense for a messenger? 🤷🏼♂️

So let’s talk about the elephant(s) in the room. 🐘🐘🐘

First off, there’s the Chinese WeChat juggernaut messenger. Anyone who has traveled to China recently will tell you that there are lots of services in China 🇨🇳 you can only pay for using the WeChat messenger 📲. So integrating a payment layer into a messenger is no science-fiction👩🏻🚀, but a model that clearly makes a lot of sense in some circumstances. Even more so, if you see that Tencent backed the Series D of Kik. 🎯

But this is not just an idiosyncratic Asian thing: most of you will know that the word is out that Facebook will be launching its own virtual currency soon. So Kik’s idea obviously wasn’t that far out there ‼️…it might have actually been ahead of its time 👾. According to a TechCrunch article from yesterday, the white paper for Facebook’s “Libra” coin will be released on June 18th and the coin will be pegged to a basket of fiat currencies 💱.

With respect to the ugly sticker set (no offense): a friend of mine recently proudly showed me his sticker collection in the Japanese LINE messenger. People pay millions for fancy emojis 🤖! No joke! Even if you’re out-of-demo for messenger stickers, it doesn’t mean that this isn’t a valid monetization model for a messenger app.

All this being said, I think issuing a token for the Kik messenger was certainly a valid product iteration overall. The SEC Commissioners might not be the target customers for the sticker set, but they might also not be the greatest HODLers of Zynga’s Farm Coins, the in-game virtual currency of Farm Ville (which to my knowledge the SEC has never challenged so far). 👩🏼🌾

Legal considerations (this is not legal advice!)

Let’s turn to the legal considerations. Being a bit of a securities regulation scholar myself, I obviously have too many opinions about the SEC to fit into a post.

But let’s not talk about the question of what should or should be regulated by the SEC in general (virtual currencies?, college education?, Kickstarter campaigns?, Tesla 3 pre-sales?) and instead focus only on some of the arguments advanced in the case.

Most of us know by now that the fate of virtual currencies is decided on the basis of a 1946 Supreme Court decision related to a Florida Citrus land baron (SEC v. W.J. Howey Co., 328 U.S. 293(1946)), which has created the now familiar Howey test 👨🏻🌾🍋👑. I let common sense decide whether this is an adequate legal authority. The test classifies a token as a security under the 1933 and 1934 Acts if there is: (1) an investment of money, (2) a common enterprise, and (3) an expectation of profits through the efforts of others.

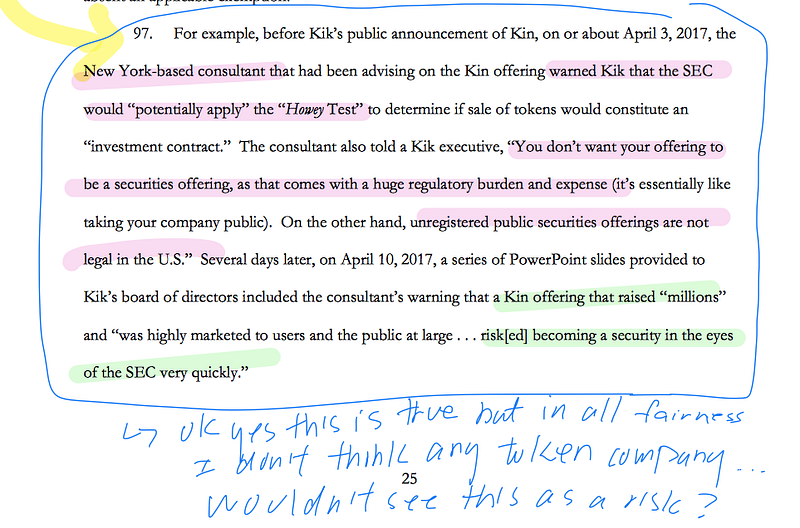

The SEC claims that Kik knew about the risk of their currency falling under the scope of the Howey test. But anyone with half a brain 🧠 or at least enough funding to hire a half-decent lawyer 👩⚖️ for a few billable hours knew that.

But to be clear: knowing about a Florida citrus grove baron case does not make you an oracle for the future regulatory actions of the Commission! ⚗️🕵🏼

But, this being said, I’m not at all surprised that the SEC is deeming Kin tokens to qualify under the Howey test. My personal opinion is that we shouldn’t regulate securities by exception to antiquated rules. Given the almost unlimited scope of the Howey test, almost anything can fall under the definition if the SEC chooses to reach for it. 🤤

I don’t want to go through all legal arguments, but highlight just a few aspects: (i) expectation of profits, (ii) foundation structure and (iii) common enterprise argument.

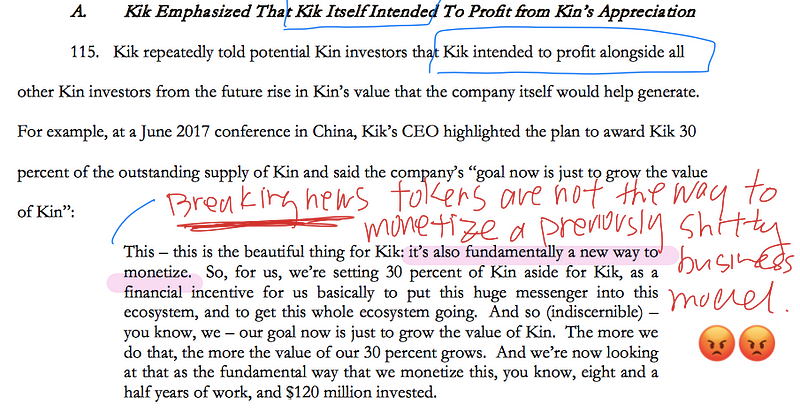

1.Expectation of profits 📈 vs. consumptive goods 🍽

Given the SEC’s extensive fact finding procedure 🕵🏼, it was able to produce lots of quotes and fact snippets to make its case on this . With respect to the expectation of profits leg of the Howey test, it relies on multiple founder interviews, such as this one:

I think no one is denying that price appreciation did not play a major role in any 2017 token offering participation. After all, this was before the 2018 stable coin hype (a topic for another day 😆).

Fred Wilson, GP at USV and board member of Kik, quoted the official Kik response in his yesterday’s newsletter, which countered this argument as follows:

“Among other things, the complaint assumes, incorrectly, that any discussion of a potential increase in value of an asset is the same as offering or promising profits solely from the efforts of another”

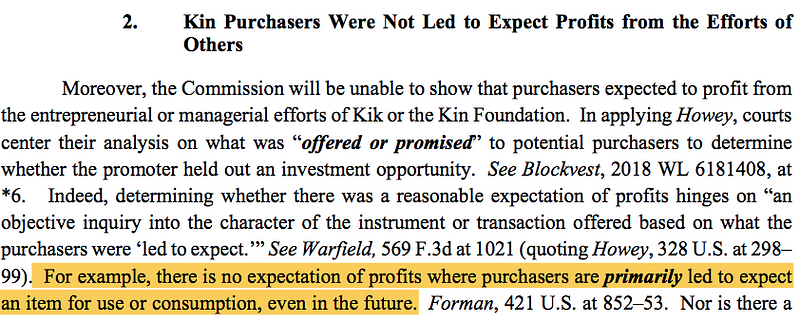

In the Wells response, the strongest argument imho rested on the consumptive nature of the tokens 🍽. In other words: you were buying the stickers not the upside. Remeber: this is why Kickstarter is regulated by the FTC and not the SEC.

I have to say, unlike for most ICOs, the consumptive case for Kik actually looks quite strong:

Kathryn Haun, who is a board member at Coinbase, a GP at Andreessen Horowitz crypto fund and a former DoJ prosecutor in a recent piece suggested how she would hone in on this if she was defending this case:

“That some participants purchased as little as 9 cents in Kin also seems more consistent with for “use” than for “investment”. If I were defending the case, I’d want to know how many people purchased such small amounts, since that is powerful evidence of a consumptive use rather than an investment. I’d also be gathering declarations from several purchasers who purchased Kik to use it with details about how they used it. It’s also entirely possible the SEC has more evidence against this argument — for all we know, they’ve interviewed dozens or hundreds of people who purchased Kin solely for investment purposes. And with 10,000 purchasers, there’s sure to be people in both categories of purchasing for investment vs. purchasing for use.”

This leg of the Howey test will certainly be highly contested and we have a lot to look forward to as this will be tested in court. In my opinion, Kik has one of the strongest cases 🤜 in the ICO space when it comes to claiming the consumptive nature. So if the consumptive good argument doesn’t fly here ✈️, I don’t want to think of some of the other projects.🔥

2.Foundation structure

Since the beginning of the ICO hype, the dominant legal architecture has relied on structuring the token sale as “donations” to newly set up foundations. I’ve always been super skeptical of this structure 🤔 and have also voiced my concerns in this respect in the past. It’s the old duck test 🦆 of:

“If it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck.”.

Some of you might remember the severe troubles that the mother-of-all-2017-ICOs, Tezos, faced with respect to its foundation governance. It’s a weak spot of the entire ICO industry though, not specific to Kik. But I’m not surprised that the SEC is going all in on trying to expose this as a weakness.

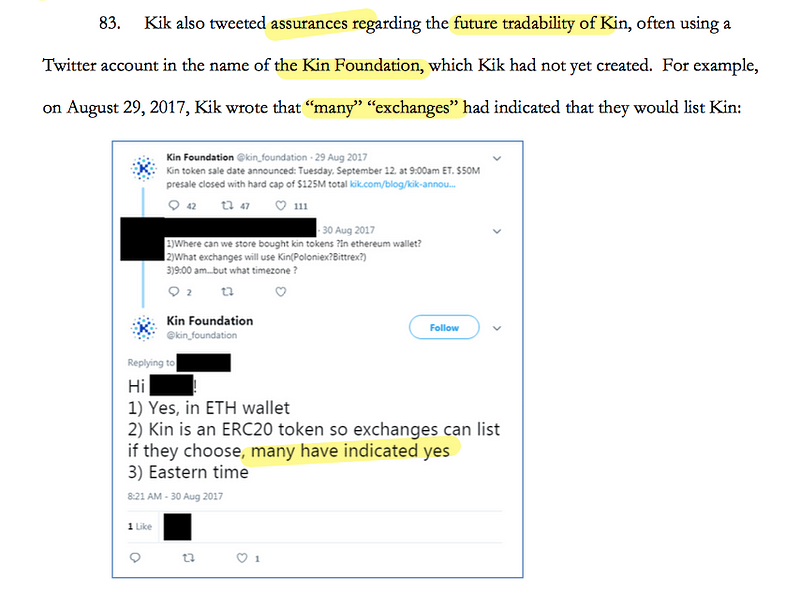

Kik apparently started tweeting from a Kik foundation twitter handle even before it had set up the foundation 🤦♂️.

This is clearly less than ideal from a governance perspective. That’s why I see such a great future for lawyers in handling social media accounts. 👨🏻⚖️🤳🏻🤣

But hey, the entire foundation structure is trying to sell off a duck 🦆 as a turtle 🐢, so I honestly don’t think that relying on a foundation structure was much of a defense in the first place. Also, it’s not specific to Kik.

3.Common enterprise

The last argument I want to discuss is that of the ‘common enterprise’. In commenting on the Wells Response, Kathryn Haun described this as the strongest argument. 🥊 I def agree with her on this.

“Kik’s best argument seems to be (2), that there’s no common enterprise between them and the Kin purchasers. Courts have held that the mere sale of something, without promising more, doesn’t give rise to a common enterprise. Based on the public information I’ve reviewed, it’s not obvious that Kik was under any contractual obligation to the purchasers other than to deliver the tokens. Once that delivery occurred, Kin holders controlled their tokens and could use them how they pleased — whether to buy items or otherwise. And plenty did. Kik created a marketplace that was open and that was meant to achieve real exchange between participants, so Kik wasn’t necessarily a participant in all transactions. Thus, the SEC may have a hard time demonstrating common enterprise between Kik and token purchasers — unless they can come up with evidence showing that Kik had obligations to purchasers after token delivery.”

In the Wells Response, it appears that the SEC has actually flip-flopped on the question of whether or not a common enterprise is required. And it seems that they did not offer any evidence to that effect for a while.

In the SEC lawsuit they do rely on the common enterprise requirement:

So the SEC is basically saying that if I co-invest with you on anything, this makes us ‘common enterprise’ 👫. Next we’ll see parents having to file S-1s if they pay for their kids’ private school? 👪🤯 I’m exaggerating of course, but this is certainly a pretty expansive definition of ‘common enterprise’ that the SEC is taking here.🎻

We don’t know what Kik will answer in this respect, in their first public response they noted:

“ Among other things, the complaint assumes, incorrectly, […] that having aligned incentives is the same as creating a ‘common enterprise”

Conclusion

The Kik case is complex. Given my bootstrapper ethos, I’ve personally become quite jaded when it comes to the entire ICO space, which has increasingly been occupied by coyotes 🐺. My philosophy has always been that “Fundraising is not a GOAL, but a SIDE EFFECT of getting traction”.

But as I pointed out the Kik case is different in many respects: product-market-fit, stage of the project and post-ICO development. Obviously, I think that we need alternatives to the attention monopolies, so I would like to see Kik and Kin succeed in one way or another. 🚀 From a macro view I think that Kik has one of the stronger cases against the SEC 🛡️ and if the SEC cracks down on this ICO, I feel the floodgates are opened and we’ll see many other project getting burned really badly soon. 🌋🔥🔥🔥🔥🔥

This is it for today.

Ttyl,

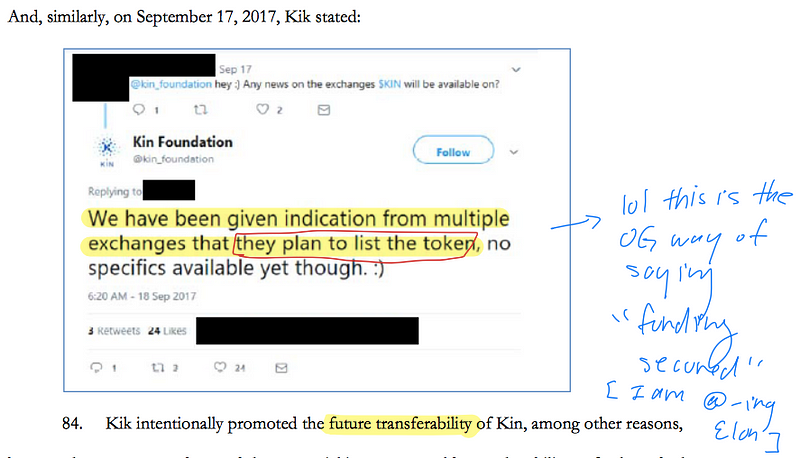

Erasmus